We have been adopting investment in bank & post office deposits as a default option without giving it much thought. At a time when interest rates were lucrative, the necessity of such analysis was also never felt. However, with the declining trend of interest rates, achieving financial targets might have become difficult. Reviewing fresh investments, adopting course correction in existing ones, and appropriate action can help achieve financial targets. The interest variation is also a risk that can hit our preconceived financial targets. The illustration below will shed some light on this aspect.

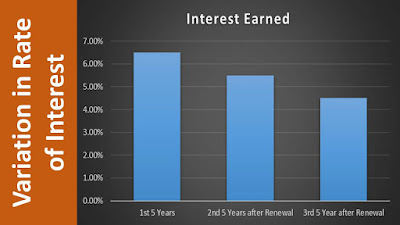

Mr. Ram & Mr. Lakhan, both started creating their children’s education fund in 2010. They set the target of Rs. 30 Lakh by 2025. Accordingly, they invested Rs. 9 Lakh in 5-year bank deposits. The rate of interest over 8.5% PA was good enough to catch the target in 15 years. However, at renewal, interest rates fell to @7.5% PA in 2015.

Mr. Ram understood the interest variation risk and diversified his investment immediately in other asset classes. With this approach, he has already crossed Rs. 22 Lakh and expects to exceed Rs. 30 Lakh by 2025, very easily.

On the contrary, Mr. Lakhan continued with the same option and opted renewal of his deposits at the prevailing rates. Now, the recent renewal in 2020, fetched just @ 5.6% PA rate of interest to conclude deposits at 25.40 Lakh on maturity, short of Rs. 4.60 Lakh from the target Mr. Ram has already crossed 25 Lakh by now & expects to exceed his target corpus by 2025.

Now, in this particular case, the investment horizon was 15 years and hence the variation in the rate of interest can’t be ruled out.

There can be two approaches –

Mr. Ram adopted the first approach and now likely to achieve his target whereas Mr. Lakhan adopted 2nd approach but did not acknowledge the interest variation risk and missed the target. Had Mr. Lakhan calibrated his investment to @ Rs. 11 Lakh, he would also be achieving the target.

Having fund protection as a prime objective, adopting the 2nd approach could be an appropriate choice but other factors can’t be ignored. However, if the horizon would have been only 5-year, the risk of interest variation could have been eliminated.

In fact, on some occasions, irrespective of the limitations offered by this investment, fund protection might be the prime concern, making them a perfect choice. But, this can’t be a default choice. Thus the investments should not follow a default choice but shall be driven by thorough analysis.

This blog shall discuss in detail, the important parameters, we must consider before adopting bank/ post office deposits as an investment.

It is worthwhile considering deposits as an investment option if our investment horizon falls within its maturity period. If our horizon is more than that of the deposits offer, we carry a risk of interest variation. Every renewal can revise the interest rates and hence the maturity value. Longer the period, the more the possibility of returns getting affected due to this variation. Hence if an investment horizon is not aligned to maturities, you must reconsider your decision.

For example – Your investment horizon is 7 years and you invest in a 5-year deposit to extend it for another two years; you are carrying a risk of interest variation. After completion of the 5th year, you may not get the same rate of interest as it is being offered now.

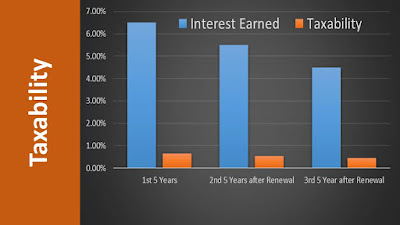

The interest earned on fixed deposits is added to the principal for the remaining period of investment but the taxability is passed on to the investor on each occasion. Hence, irrespective of the interest credited to your account you become liable to pay taxes on such interest. This becomes an additional burden in terms of tax. But on the other hand, this could be a blessing also, if your income remains within zero tax brackets even after adding this interest. The interest, at maturity, can probably push you to the next tax slab, but its distribution across the beginning to maturity period, may not.

For example – If the interest earned at maturity is Rs. 2.5 Lakh, one-time inclusion in taxable income might push you to the next higher tax slab. But when it is distributed across a 5-year term, its impact is only Rs. 50,000 per year, that might not be enough to push you to the next higher tax slab.

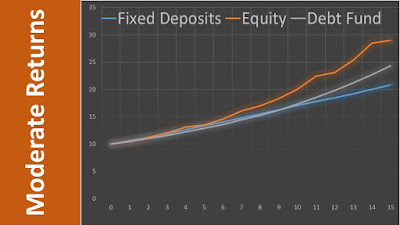

The fixed deposits grow at a moderate rate. This normally floats with a generic inflation rate but absolute returns are further discounted by taxes. But this moderate growth is rewarded by higher security compared to other debt instruments. This security is extended through their insurance. Since deposits are insured to a certain value only, they still carry a little risk. However, this risk can be reduced by distributing the deposits to multiple banks. If high growth is not a driving factor but fund protection is a major concern, fixed deposits become a good choice.

The fund invested remains locked for the period it is invested. Although part withdrawal in the form of a loan, fore-closure with a penalty are the options available to handle liquidity yet a financial loss is inevitable. Hence you must consider this aspect if selecting this option for investment. If liquidity is a foremost requirement, plan your deposits (breaking in many FDs in terms of values and duration) appropriately, to handle this aspect.

For example – If you want liquidity of the corpus in five consecutive years, break the corpus in such a way that every year, one deposit of desired value attains maturity.

Conclusion

Bank or Post Office deposits are widely used investment options having the reach to the smallest villages. But the dynamics of the financial market not only affect equities but also all financial instruments and debt-based products are not the exception. An analysis of all the features of any financial product helps to understand the risks & returns associated with it. Deposits also carry interest variation risk/ liquidity risk etc. and thus shall never be considered as riskless. Hence while selecting this, as an investment option; this should be a cautious decision rather than an obvious decision.